Box Inc.: Still an Acquisition Target

Despite KKR's recent equity infusion, a Box sale is still possible

Author’s note: This analysis was finalized on April 7th. The following day, on April 8th, KKR announced a $500M convertible preferred equity investment in Box. Box plans to use the proceeds in a Dutch auction style share buyback program. The buyback may alleviate pressure from activist shareholder Starboard Capital to pursue a sale process. Starboard’s decision to participate in the buyback remains to be seen and Box may still attract interest from other activist funds, private equity firms, or strategic buyers. Therefore, I believe much of the analysis remains valid.

Recommendation

Box Inc. (NYSE: BOX) is fairly valued at its April 6th closing price of $24.11. However, the stock is a buy over the short and medium terms due to recent, credible rumors that Box Inc. may be an acquisition target.

Company Background

Box Inc. (the Company) is a cloud based, software-as-a-service (SaaS) platform that allows for the storing, sharing, and editing of nearly any type of digital content. Box’s customizability, compatibility with a wide variety of devices and operating systems, and ability to integrate with over 1500 third party applications (Microsoft Teams/Office, Zoom, Salesforce etc.) allow it to serve as an organization’s internal and external collaboration medium, or “single source of truth.” The Company sells sophisticated data security, encryption, and tracking/auditing technology, and offers add-on services such as local data storage, no code workflow automation functions, and industry specific regulatory compliance tools.

Unlike many other individual user focused cloud content management competitors, Box targets organization and enterprise level adoption with largely non-cancellable, periodically invoiced, one to three year contracts. Paying customers- across 105,000 organizations- comprise 20% of the Company’s 77.7M registered users (seats). Non-U.S. customers, primarily in Japan, account for 28% of revenues. Revenue in FY 2021 ending January 31 was $770.8M (up 10.7% YoY, 14.1% 5 year CAGR), with a 70.8% gross margin and operating loss (including stock based compensation) of $37.6M. Despite consistently strong and improving cashflows (CFO less CapEx of $187.8M in FY 2021), Box has never turned a profit.

Current Status

Box operates in the hyper competitive “cloud content” space. The Company is constantly jockeying for market share with peers such as Dropbox and OpenText Corp, tech giants Google (Drive) and Microsoft (Teams), and stubbornly entrenched, legacy enterprise systems such as SharePoint. Box has a user-friendly UI, compatibility with nearly every major productivity software application, and a sizable base of large customers that are increasingly anchoring themselves in the Box ecosystem by adopting add on product offerings. This latter trend is expected to lower sales and marketing costs as cross selling is generally cheaper than new customer acquisition. Box also plans to release a highly requested e-signature feature this summer and expects to benefit from COVID structural tailwinds as firms boost IT spending(1) to accommodate a dispersed workforce.

However, for a SaaS company (albeit one that management insists does not have the luxury of selling into unencumbered, greenfield markets), growth remains frustratingly low (projected revenue growth of 14% by FY 2024) with high corresponding sales expenses to achieve that growth (stock-based compensation alone is 20% of revenue). Despite Box’s presence in many firms and opportunity to upsell existing clients (management sees 7x possible additional “seats” from current customers), there are limited barriers to entry to the cloud content management space. Google and Microsoft pose an especially pertinent threat given their dual advantages of ubiquity and ability to offer a similar product as a loss leader for low or even no cost.

Investment Thesis

Box is a prime acquisition target for either a financial or strategic buyer. The Company has proven technology, branding, and usage from top tier, enterprise customers, but suffers from anemic growth (when compared to other SaaS names) and lacks sufficient scale to defend against potential challenges from Google, Microsoft, or other legacy tech titans.

Acquisition Discussion

Because Box is designed to be used across an organization and engage with a diverse array of third-party applications, it can appeal to a range of strategic buyers- from file sharing firms like Dropbox to “cloud” based providers such as Amazon Web Services to a long list of general enterprise software firms (Adobe, Salesforce, Microsoft etc.). A financial acquisition and turnaround- along the lines of the highly successful Vista Equity Partners purchase and 2018 sale of Marketo to Adobe- are also conceivable with the Company having a middle market sized EV of $3.89B, minimal debt, and opportunities to lower expenses- particularly in its costly sales force.

Starboard Value, a well-known activist hedge fund, took a 7.9% stake in Box in late 2019 and currently controls three seats on the nine-person board. Three more seats, including CEO Aaron Levie’s, are up for election this June. Starboard has privately expressed interest(2) in obtaining these additional seats(3). If the hedge fund were to command the majority of the board, there becomes a much greater likelihood of a sale or drastic company reorganization (with the possible ouster of founder CEO Levie and co-founder, and childhood friend, CFO Dylan Smith).

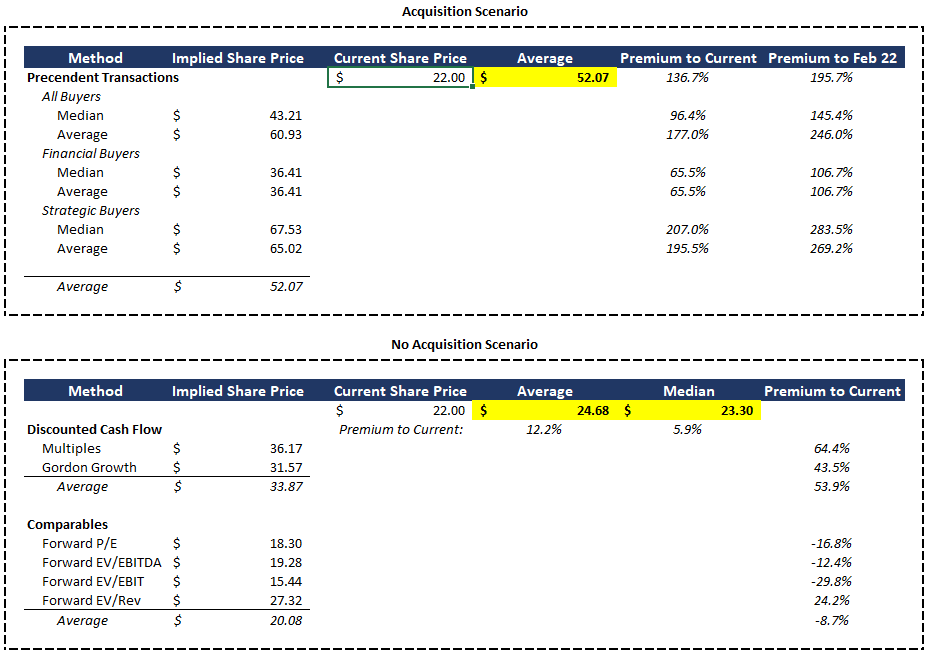

Based on 15 enterprise software company acquisitions over the past three years with transaction values between $2B and $8B, Box could fetch a price of $52 a share- a 116% premium to the April 6th close. Within this deal cohort, financial buyers have offered a 51% premium (implied Box share price of $36) and strategic acquirers have paid 175% above market (implied share price of $66). As Box is an attractive target to a multitude of buyers, any sale process would likely be highly competitive- further driving share price premiums.

Risk Factors

An acquisition does not materialize, or Box is acquired for a discount or immaterial premium to its current share price.

Given the Box’s underperformance since its IPO and unremarkable outlook, Starboard Value has a reasonable chance in succeeding in its board seat challenge (and directly soliciting a sale) or pushing management to shop the Company. A significant premium is expected based on precedent transaction implied prices and Box’s attractive business dynamics drawing several competitive financial and strategic bidders.

Large tech competitors enter and launch a cloud content management product for low or no cost

While Box would not be able to compete on price, the Company has several features that make its product “sticky” or highly attractive to customers. These features include Box Sign (E-signatures) and Box Shuttle (facilitates easy content migration and adoption of the Box platform) among others.

Box links many different applications from various software firms and does not provide content creation tools (e.g. Google Docs or Microsoft Office)- benefiting from being a “neutral” third-party without a perceived conflict of interest or favoritism of a certain application.

Incumbent enterprise systems prove too expensive and difficult to displace

Box sells to firms that often have deep-rooted, legacy enterprise sharing software that requires considerable amounts of time, integration expenses, and credibility with the customer to fully replace with the Box platform. Box is aware of this and has been directing much of its sales efforts toward the easier/cheaper route of cross selling existing customers. The Company has also released products such as Box Shuttle that are designed to streamline the integration process.

Regulatory compliance costs make expansion prohibitively expensive

Regulatory action remains highly uncertain. However, acts such as the European Union’s General Data Protection Regulation (GDPR) and the California Consumer Privacy Act (CCPA), both of which govern the handling of personal data, may entail additional Box R&D and legal expenses to remain compliant. Again, this is speculation and the full impacts of the acts have yet to be seen.

Box is not acquired and continues to experience lackluster growth and no near-term path to profitability

Box is cashflow positive, offers a well-regarded product that is used by 68% of the Fortune 500, and expects expenses to decrease as the Company upsells existing customers. There are no visible near-term liquidity or solvency risks and the post-COVID, dispersed workforce, heavy IT-spending, macroenvironment is supportive of the Box product.

Valuation Summary

1. Evercore ISI's Quarterly Enterprise Technology Spending Survey (Q1 2021)

2. As reported by Reuters on February 23rd, 2021: Link

3. RGM Capital, another activist known for agitating for change, also has a 4.7% stake