The Barbell Brokerage

YOLO Invest Responsibly

The State of the World

Last week, Robinhood Markets Inc. released its first quarterly earnings as a public company. To the surprise of no one, the filing generally cemented the app’s long held reputation as a gambling platform. Robinhood’s two largest sources of Q2 revenue are transactions fees (spreads, payment for order flow [PFOF] etc.) from highly speculative options trading ($165M) and cryptocurrencies ($233M).

Crypto represented 41% of total revenues. Of that 41%, 62% came solely from Dogecoin trades. This means an absolutely appalling 25%, or $143.7M, of all revenue came from a digital coin based on a 2013 meme that the original creator coded in a few hours on a Sunday afternoon as an explicit joke. This has been well documented elsewhere and I do not need to rehash the financial media coverage. I only highlight it because:

It is objectively hilarious (and certainly a bit sad).

The options and crypto focus is the most obvious example of Robinhood (and other upstart brokerages) capitalizing on the oft reported YOLO culture of investing and financial “planning” of the Millennial and Gen Z cohorts.

Younger people tend to be more risk seeking and have a greater ability to bear risk with longer time horizons to recoup losses. As Robinhood has demonstrated, providing the means to take these risks is quite lucrative. This is nothing new: running a casino without having to pay rent or give out free drinks is a good business. So, the younger generation wants to gamble- until they blow up on some insane leveraged trade- and the brokerages want to offer the means to do so- until they are either the subject of a Congressional hearing and are regulated to death or face credible bodily threats from disgruntled users.

Robinhood co-founders Baiju Bhatt and Vlad Tenev on IPO day, with at least three visible bodyguards

This situation, whatever it is, is not sustainable and should not be maintained. That said, we do not need to pursue an abstinence only policy whereby we eliminate risky trading. Instead, we should embrace it in a managed way with the “Barbell Brokerage.”

What is the Barbell Brokerage?

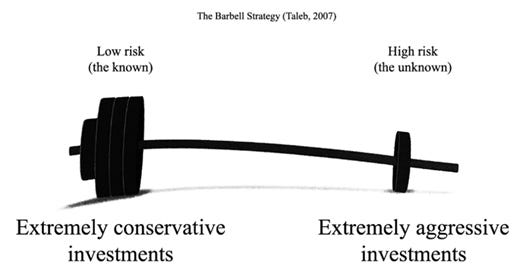

“Barbell Investing” describes an investment philosophy that dictates a portfolio’s optimal risk and return profile can be achieved by purchasing assets that are either extremely risk or carry no risk at all. A simplified example would be an allocation to pre-revenue, highly volatile biotech companies, with the rest of the portfolio being in risk-free treasuries. Assets with moderate risk and return figures- blue chip stocks, investment grade bonds, etc.- are omitted. Depending on the weighting, a barbell approach can theoretically generate a portfolio that sits on the very-much-a-textbook-idea efficient frontier (or close enough to it).

Why not apply this concept to a brokerage? Instead of hopelessly trying to encourage investors to buy and hold a widely diversified basket of stocks and bonds while telling Robinhood & co. that they should not promote excessive trading in risky assets (which is the equivalent of saying “stop making money”), segregate the brokerage into two sleeves: the (Jack) Bogle Bucket and the YOLO ‘Folio.

Bogle Bucket

As the Vanguard founder’s name implies, the Bogle Bucket consists exclusively of low-cost, boring index funds. Choices range from 60/40 mixes to target date funds to income strategies to, for the extra adventurous, Russell 2000 small cap ETFs. Ideally, an algorithm generates a personalized portfolio based on a user submitting her personal balance sheet, income, risk tolerance, liquidity needs, time horizon etc. Income would be automatically reinvested pro-rata unless the user specified otherwise.

To discourage spontaneous or myopic panic trading, selling is intentionally made cumbersome, though there is no contractual lock up period. For example, users might be prompted to confirm they do in fact want to sell and asked why and what they plan to do with the funds. None of this needs to be answered or approved by the brokerage. The goal is to slow down the decision-making process and ensure that the sale is a prudent, long-term decision. Additional psychological tricks might include calculating and displaying the approximate tax impact and giving the user estimates of lost lifetime earnings if she were to divest.

Revenue generation comes from a combination of a low basis point fee on total assets, additional charges for customized financial planning, interest on cash, and perhaps some quasi-banking products such as lending origination or buy now pay later services.

By design, there is nothing earth-shattering here. At least 90% of a user’s assets would sit in this bucket, accumulating and compounding overtime into a promising retirement fund.

YOLO ‘Folio

On the other end of the barbell, YOLO ‘Folio could have one of two basic structures.

The first is mostly a replica of Robinhood that omits some of the app’s more absurd features, such as trading on margin: no one needs to be taking on leverage to buy (inherently) leveraged options. Single stocks, options on equities and funds, crypto, NFTs, sports betting, even some binary outcome event-based trading as seen in platforms such as PredictIt and Kalshi are all fair game. Revenue comes from the infamous payment for order flow mechanism (which actually offers the retail customer a better deal than directly routing order to the exchange, but that is beyond the scope of this piece). Users are welcome to go nuts here. It would even reinstate the digital confetti.

The second framework still allows the user to trade the above-mentioned instruments, but there are more self-governance tools- such as a self-imposed “time out” rule that limits a customer to paper trading for a defined period if losses fell below a certain threshold- and, most importantly, a flat commission in lieu of PFOF. Whether or not it is economically rational (i.e. the fee is openly displayed rather than buried in the PFOF system), the commission component would likely deter excessive trading- a major source of investor loses due to the “buy high, sell low” emotional trading tendency. From a marketing perspective, commissions are a feature, not a bug: the customer is paying for best execution and is not beholden to high frequency traders or hedge funds front running her orders or distorting markets (again, irrespective of how true that is).

All of this is to relegate the inevitable gambling portion of today’s investing into a small, and easily managed walled garden. By keeping the bulk of the user’s attention on the YOLO ‘Folio- and the bulk of the assets in the Bogle Bucket- fun is had and catastrophic losses are minimized. The platform providing the Barbell Brokerage could have a strong revenue model that benefits from the lucrative, but volatile and controversial brokerage business and the more stable, out-of-the-regulatory crosshairs robo-advisory, wealth management vertical. It is time to acknowledge that “abstinence only” is not viable for today’s trigger-happy investors and trade volume-dependent brokerages. We can be smart about being dumb.

Addendum

There are countless other features that could be added to this structure to either increase revenue or nudge users to certain behaviors. A few that come to mind include back tests on customer’s portfolios (e.g., if you did not make this trade your performance would have been X% higher), charging additional fees for more advanced Bogle Bucket strategies like tax loss harvesting or covered call writing, selling advertising space or data to third parties, making owed taxes readily apparent, and even a social component akin to the Public app or prize based leader boards for paper trading competitions. The possibilities- subject to considerable A/B testing- are endless.